What Are Commercial Collections?

If you’re running a collection agency, chances are most of your work is tied to consumer debt collection—credit cards, auto loans, or medical balances. But commercial debt collection is a different world entirely.

Commercial debts involve one business owing another. Think unpaid invoices, broken contracts, or overdue receivables from a customer who’s also a supplier or distributor.

Unlike consumer accounts, commercial collection agencies don’t operate under the Fair Debt Collection Practices Act (FDCPA). That means fewer restrictions on phone calls, text messages, and demand letters. But it also means higher expectations— because the creditor usually wants to preserve the relationship. After all, the debtor might still be an important client.

Why Agencies Consider Adding Commercial Debts

Higher Balances, Bigger Opportunities

Consumer accounts might average a few hundred or thousand dollars. Business debt balances often stretch into the tens or hundreds of thousands. That means more revenue per account, and potentially faster improvements to client cash flow.

Diversification Against Market Swings

Consumer delinquencies rise and fall with the economy. By offering collection services for both consumer and commercial debts, agencies stabilize their book of business and reduce risk.

Stronger Client Relationships

Creditors don’t just want debt recovery—they want to protect customer relationships. Agencies that handle commercial debts professionally become trusted long-term partners.

Challenges of Commercial Collections

A Different Collection Style

With consumer accounts, persistence (within FDCPA limits) often drives results. With commercial collectors, the style shifts: professionalism, negotiation, and documentation matter more than repetition.

- A demand letter needs to be firm, but not aggressive.

- Telephone calls should be treated as business-to-business negotiations, not pressure tactics.

- Preserving the attorney–client relationship is crucial if cases escalate to a law firm or collection attorney.

Complex Disputes

Unlike consumer debt, commercial debts often involve disagreements about services, contract terms, or product quality. Your team must be able to handle these disputes tactfully while keeping recovery on track.

Legal Escalation

Many commercial cases end up requiring legal action. Your agency will need escalation workflows that involve attorneys, proper documentation, and airtight audit trails.

What Your Agency Needs to Compete

Train Commercial Collectors

Your collectors aren’t just debt collectors—they’re negotiators. They need to understand contracts, payment terms, and the nuance of protecting relationships while pushing for resolution.

Upgrade Your Tech Stack

Commercial clients expect visibility. If your collection process still relies on manual reporting, you’ll lose credibility. Modern debt collection software should provide:

- Client portals with live dashboards on receivables

- Automated payment plan scheduling and dispute tracking

- Omnichannel outreach (email, text, LinkedIn, and calls)

- Built-in compliance for state laws, even if FDCPA doesn’t apply

Learn more: Top Debt Recovery Software Features for Agencies in 2025

Structured Escalation

Have a clear ladder for your collection efforts:

- Friendly reminders and text messages

- Formal demand letters

- Engagement with a collection attorney

- Legal action through a partner law firm

When workflows are automated, your team can manage higher volumes of both consumer and commercial accounts without ballooning headcount.

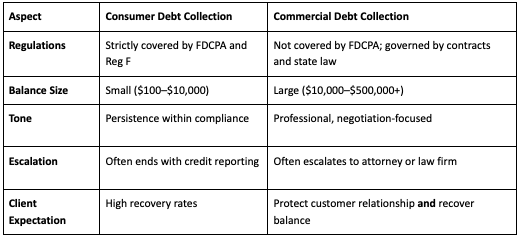

Consumer vs. Commercial Debt Collection

When comparing consumer vs. commercial debt collection, the differences go far beyond just account size. Each type has its own rules, tone, and client expectations.

Consumer collections are shaped by strict federal regulations, while commercial collections lean more on contracts, negotiation, and relationship management. Here’s a side-by-side breakdown to help you see the contrasts clearly:

Is Your Agency Ready?

Signs You’re Ready

- Existing clients ask about commercial collection services

- Your software supports segmentation, high-volume accounts, and portals

- You have or can partner with collection attorneys for escalations

Red Flags

- Still using legacy tools with no automation

- Collectors only trained on consumer debt collection scripts

- No access to legal partners or law firms for advanced cases

Key Takeaways

- Commercial debt collection offers bigger balances and stronger client relationships, but requires a different playbook.

- The collection process is less about FDCPA restrictions and more about negotiation, documentation, and professionalism.

- Agencies need modern collection methods—AI-driven outreach, portals, and escalation workflows—to compete with established commercial collection agencies.

- Success means preserving relationships while recovering outstanding debts quickly and efficiently.

Final Thoughts: Growth Without Guesswork

Adding commercial collections isn’t just about chasing bigger accounts—it’s about proving to clients that your agency can handle complex, high-value receivables with professionalism.

Agencies that rely on outdated systems and manual workarounds will struggle. Agencies that invest in modern automation, AI outreach, and real-time reporting can expand into this market confidently—and win.

👉 Next step: Book a demo with Aktos to see how modern tools simplify both consumer and commercial collections in one platform