Debt collection AI is only as useful as the account context it can trust.

That is where many automation projects break down. Agencies often focus on the visible AI layer first: AI agents, AI collection agents, call summaries, queue scoring, or automated workflows. Those tools matter. But if they are running on stale balances, missing dispute notes, outdated consent records, or disconnected payment history, the agency is not automating intelligence. It is automating bad assumptions.

For enterprise collection agencies, real-time data quality is not a technical preference. It determines whether debt collection AI improves recovery rates, protects compliance, and supports better debt recovery, or creates more cleanup for collectors, supervisors, and client services teams.

What Clean Account Context Means for Debt Collection AI

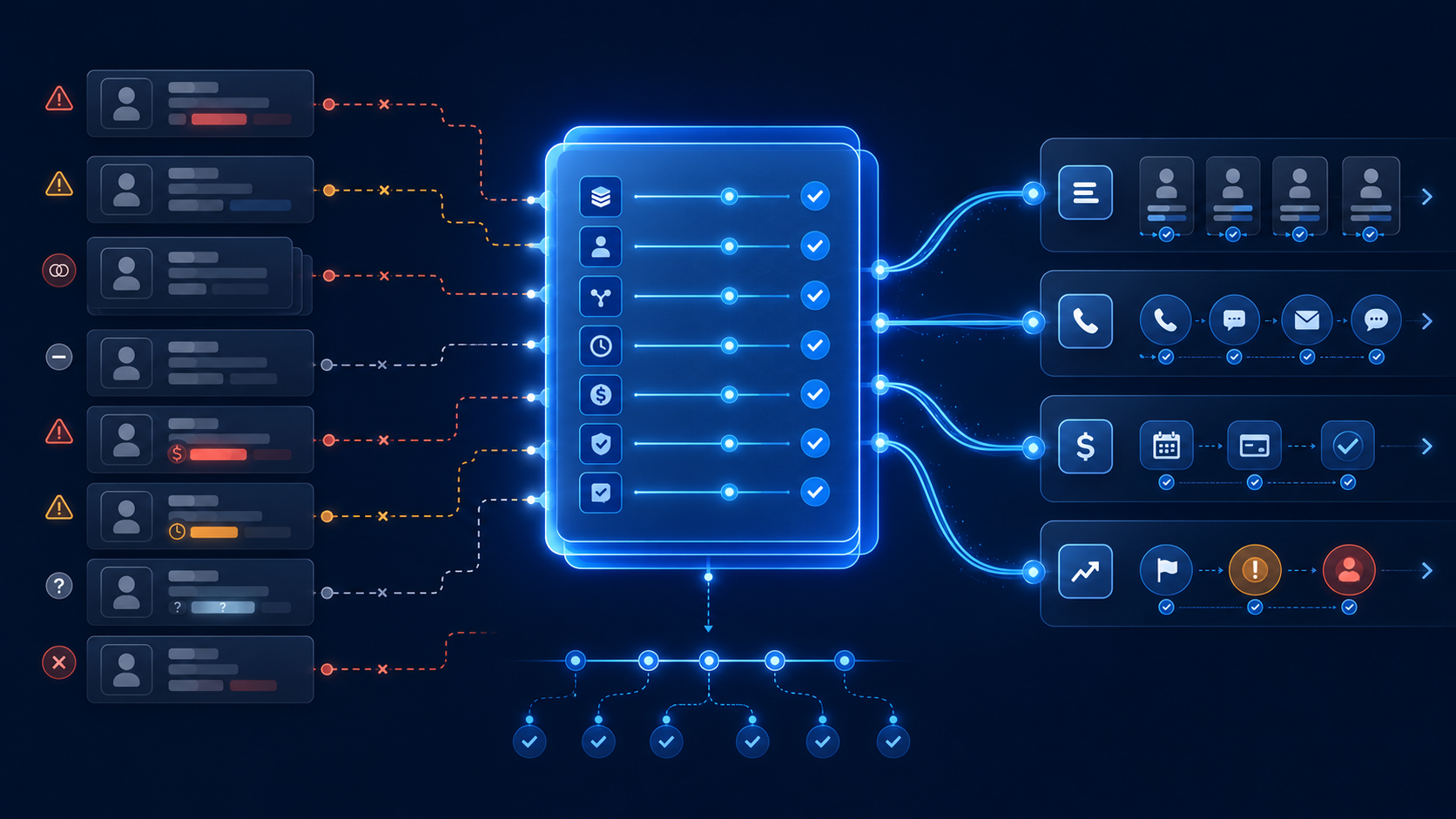

Clean account context means the system has current, structured, usable information about the consumer, account, compliance status, communication history, and workflow stage. It is not just “data in the CRM.” It is data that AI agents can safely use before they act.

For debt collection AI, that context may include:

Current principal balance, fees, and payment status

- Recent payments, reversals, failed payments, and payment plans

- Disputes, verification requests, and dispute resolution status

- Consent and revocation status by channel

- Phone, email, address, language, and contact preference data

- Prior call outcomes, sentiment analysis, and conversation summaries

- Client-specific rules, portfolio rules, and workflow ownership

- Compliance controls for FDCPA, TCPA, Reg F, and state requirements

- When this information is accurate, AI can support smarter debt recovery decisions. When it is stale, even strong AI debt collection software can trigger the wrong outreach, recommend the wrong next step, or route an account before it is eligible.

Why Stale Data Creates Bad Automation

A human collector may notice when something looks off. An automated workflow will usually follow the data it is given. That makes data freshness especially important in consumer debt workflows.

If a consumer made a payment through a portal but the account has not synced, an AI phone agent may still follow up as though the balance is unpaid. If a consumer revoked SMS consent but that update sits in a separate messaging tool, the next automated message can create TCPA risk. If an account is in dispute but the status is delayed, normal outreach may continue when the account needs a different treatment path.

The problem is not that automation failed. The problem is that automation trusted outdated context.

This matters because AI affects more than call volume. It can influence prioritization, payment reminders, debt resolution paths, supervisor alerts, and client reporting. If the underlying data is wrong, the output looks efficient but still creates consumer friction, compliance exposure, and lower recovery rates.

The Data AI Agents Need Before They Act

Different AI use cases require different context, but several categories matter across most collection operations.

Payment and Account Status

AI should know whether an account is unpaid, partially paid, paid in full, on a payment plan, in settlement, pending reversal, or recently updated. It should also understand the principal amount and current status before suggesting payment options.

This is especially important when agencies support ACH, cards, text-to-pay, recurring payment plans, debtor portals, and client-side updates. Payment history must move quickly into the collection platform so AI agents do not chase accounts that have already changed.

Disputes, Verification, and Compliance Signals

If a consumer disputes a debt or requests verification, the workflow should change immediately. AI needs to know when the dispute came in, which documentation exists, who owns the next step, and whether outreach should pause, change, or escalate.

The same is true for FDCPA, Reg F, TCPA, PCI-DSS, and state-level controls. The FTC’s FDCPA text and CFPB Regulation F show why collection workflows need rules-aware communication controls. For payment-related workflows, the PCI Security Standards Council is a useful reference point for payment-data security expectations.

Communication History and Preferences

Modern collections are omnichannel. A consumer may receive an email, click a portal link, miss a call, reply to an SMS, and then call after hours. Conversational AI and natural language processing can help summarize these interactions, but only if the communication history is unified.

A good AI workflow should know what has already happened, which channel is allowed, what language the consumer prefers, and when human escalation is appropriate. Otherwise, the experience feels fragmented: repeated questions, duplicate reminders, or outreach that ignores prior context.

How Machine Learning and Predictive Analytics Depend on Data Quality

Machine learning and predictive analytics can help collection agencies prioritize accounts, forecast engagement, and identify patterns in payment behavior. But machine learning models are only as reliable as the data feeding them.

If resolved accounts remain active, if debt settlement outcomes are logged inconsistently, or if payment histories are split across CRMs and payment processors, the model learns from noise. That can affect credit score-related segmentation, credit rating context, collector queues, and recovery strategy.

The same issue applies across account types. Credit card, healthcare, telecom, debt consolidation, buy-now-pay-later, and other consumer debt portfolios all have different behavior patterns. A debt consolidation account may need a different context than a buy-now-pay-later balance. Older bad debt may require different treatment than newer placements. AI should not flatten those differences into one generic workflow.

Where Legacy Systems Struggle

Many legacy collection systems were not built for real-time AI workflows. They may rely on batch updates, manual imports, limited APIs, bolt-on dialers, disconnected portals, or delayed reporting. Those gaps become obvious when agencies try to deploy AI agents at scale.

A disconnected stack can make the agency look automated on the surface while back-office teams still reconcile records manually. One system has the payment update. Another has the consent change. Another has the call recording. Another has the client reporting data. The AI can only act on the context it can actually access.

That is why AI strategy and platform strategy need to work together. Agencies should not only ask whether a tool can automate calls. They should ask whether it can access the right account data, apply the right rules, update the record, and coordinate with every other workflow.

What to Look for in Automated Debt Collection Software

Automated debt collection software should make AI safer and more useful by keeping data connected. When evaluating AI debt collections software or broader debt collection software, agencies should look for:

Real-time or near-real-time account updates

- Integrations across CRMs, dialers, payment processors, portals, credit bureaus, and client systems

- Audit trails for payments, disputes, consent, communications, and workflow changes

- No-code rules for automated workflows and exception handling

- Dashboards that surface stale records, failed syncs, and workflow bottlenecks

- Security and role-based access controls for sensitive data

- Agencies should also know which privacy frameworks actually apply.

How Aktos Supports Real-Time Collection AI

Aktos is modern, AI-powered debt collection software built so automation works inside the collection workflow, not beside it. With integrated communications, open APIs, no-code workflows, real-time dashboards, and connected account records, Aktos helps agencies give AI the context it needs before it acts.

That matters because AI in debt collection is not just about automation. It is about using AI agents, generative AI, NLP, predictive analytics, and operational data together in a controlled system. For compliance-heavy use cases, agencies should also understand how AI phone workflows interact with consent, call timing, disclosures, and escalation rules, which Aktos covers in its guide to AI phone agent compliance.

Final Thoughts: AI Needs Context Before Autonomy

The future of debt collection AI is not simply more automation. It is better contextualized automation.

Enterprise agencies that invest in real-time data quality are better positioned to use AI safely and effectively. They can reduce duplicate outreach, improve debt recovery workflows, support stronger compliance operations, and give clients more confidence in reporting.

AI can help agencies scale. Clean account context is what keeps that scale under control.

FAQs

Q: What data does debt collection AI need most?

A: Debt collection AI needs current payment status, payment history, dispute status, consent data, communication history, account ownership, workflow stage, and compliance rules before taking action.

Q: Can AI improve recovery rates?

A: Yes, AI can support better recovery rates when it uses accurate data to prioritize accounts, personalize outreach, route consumers, and automate follow-up. Poor data can undermine those gains.

Q: Is AI debt collection software compliant by default?

A: No. Agencies still need compliant workflows, legal review, consent tracking, audit trails, and controls for FDCPA, TCPA, Reg F, state rules, and applicable payment security requirements.

Q: How is AI used in debt resolution?

A: AI can help identify next steps, summarize conversations, support payment plans, route disputes, and escalate sensitive accounts to humans. It should not replace documented policy, legal judgment, or human oversight.