Regulation F Isn’t Enough for Compliance

If you're a leader at a third-party debt collection agency, navigating the landscape of regulations can feel overwhelming. You’ve studied Regulation F. But here’s the catch: just following it alone won’t keep your agency compliant in most states. If you’re collecting debts across borders, you’re juggling dozens of rules—and one slip could cost you a client. The surprising truth is that Regulation F alone won't fully protect your agency when collecting debts. Here's why.

Understanding Regulation F: Your Federal Baseline

In 2021, the Consumer Financial Protection Bureau (CFPB) introduced Regulation F as part of the Fair Debt Collection Practices Act (FDCPA), significantly modernizing debt collection practices. Published in the Federal Register, the final rule established clear guidelines around call frequency, validation notices, and electronic communications.

Key Components of Regulation F:

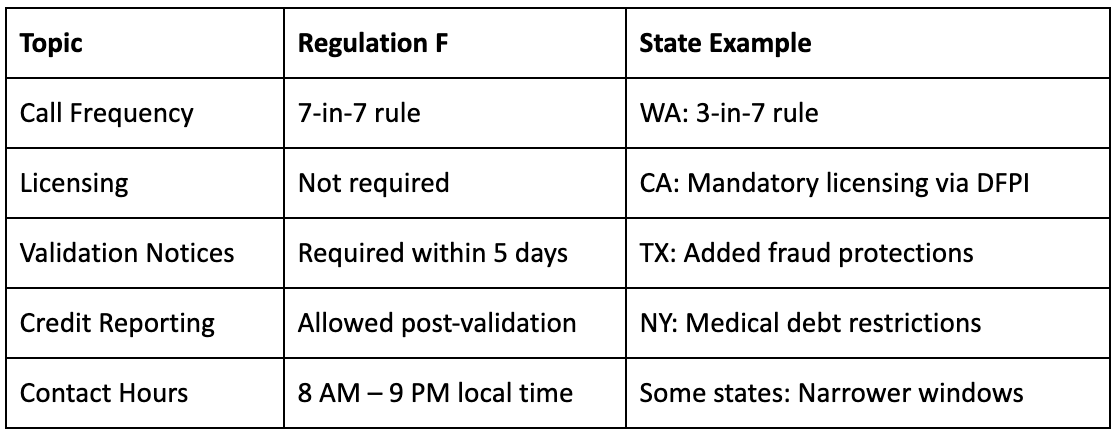

- Call Frequency Limits: The "7-in-7" rule limits debt collectors to seven telephone calls within seven days per consumer.

- Validation Notice Requirements: Debt collectors must provide clear validation information during initial communication or within five days.

- Electronic Communications: Regulation F explicitly allows electronic communications, including text messages, emails, and social media, but imposes strict compliance requirements.

- Limited-Content Messages: Introduces a safe harbor for voicemail messages that avoid revealing sensitive debt information beyond a telephone number.

Where Regulation F Falls Short: Detailed State Law Comparisons

Regulation F provides a robust federal framework for consumer protection, but individual states often introduce stricter or unique new regulations:

Call Frequency: Washington vs. Regulation F

- Regulation F: Allows seven contact attempts per week.

- Washington State: Stricter "3-in-7" rule, limiting collection agencies to just three contact attempts within a seven-day period.

Licensing and Registration: California & New York vs. Regulation F

- Regulation F: No licensing or registration requirement.

- California: Requires agencies to obtain licensing through the Debt Collection Licensing Act.

- New York: Mandates registration with the Attorney General and imposes additional restrictions on credit reporting, particularly medical debts.

Debt Validation Notices: State vs. Federal

- Regulation F: Standardizes validation notice requirements to clearly communicate consumer rights, original creditor details, and debt specifics.

- California: Requires additional disclosures for consumers impacted by scams or identity theft.

- Texas: Imposes rules against misleading representations, requiring careful attention to validation notices.

Failing to adhere to these nuances can result in costly compliance breaches.

Where Reg F Stops—and States Take Over

Here’s the part many agencies miss: states can (and do) make the rules stricter. And your agency is on the hook for both.

Fall out of bounds on any of these? You’re risking lawsuits, fines, and client churn.

Compliance Errors Can Derail Growth

In debt collection, even small compliance missteps can have outsized consequences. State attorneys general and federal regulators like the CFPB and FTC are increasingly aggressive in enforcement, and agencies that overlook rule changes or state-specific nuances often find themselves facing fines, lawsuits, or strained client relationships.

With regulators scrutinizing everything from call frequency to credit reporting practices, modern agencies need software that enforces compliance in real time—before issues escalate into liabilities.

Learn more: Modern Debt Collection Solutions | State Laws Agencies Must Know

One Missed Rule. One Lawsuit. One Client Lost.

Compliance isn’t just about avoiding fines. It’s about credibility.

Every time your collector calls too often, sends the wrong notice, or fails to register in a state that requires it, your agency’s brand takes a hit. Clients notice. Regulators notice. And once you're on their radar, it’s hard to get off.

Even small compliance slip-ups can lead to:

- Regulatory penalties from the CFPB, FTC, or state AGs

- Consumer disputes and chargebacks

- Contract issues with clients demanding indemnity

- Reputational damage you can’t walk back

Leveraging Technology for Multi-Jurisdictional Compliance

Modern compliance isn’t a checklist—it’s a system. Legacy software forces your team to patch together rules, remember state-specific contact caps, and manually update documents. That’s not scalable. And it’s definitely not safe.

Here’s how modern platforms like Aktos keep your agency compliant—without manual workarounds:

Automating Compliance with Aktos

- State-Based Logic Automation: Automatically adjusts call caps, disclosures, and validation requirements based on the consumer’s state. No more “hope we got it right” moments.

- Unified Omnichannel Communication: All outreach—SMS, emails, voicemails, letters—is logged, time-stamped, and linked to the account. Every state’s communication rules? Already baked in.

- Real-Time Compliance Dashboards: Instant alerts show you when collectors are approaching limits or missing required steps. No waiting for a monthly audit to catch problems.

- No-Code Workflow Builder: Your ops team can launch new rules, templates, and triggers—without touching code or waiting for dev. Perfect for when states update their laws mid-year.

Learn more: Top Debt Recovery Software Features for Agencies in 2025

Best Practices for Comprehensive Compliance

Here’s how top agencies stay ahead and avoid compliance pitfalls:

- Regularly Update Training: Inform your team about changes in federal rules, CFPB advisory opinions, and state laws.

- Monitor Trusted Sources: Regularly visit the official website of the United States government, consumerfinance.gov, and other reliable sources.

- Invest in Compliance-Focused Technology: Leverage platforms with automated compliance and audit capabilities to reduce human error and streamline operations.

Frequently Asked Questions (FAQs)

Does Regulation F supersede state law?

No. Regulation F sets a federal baseline, but states can enforce stricter consumer protections. Agencies must comply with both.

What if Regulation F and state laws conflict?

Always adhere to the stricter standard to avoid potential penalties or lawsuits.

How often should we refresh compliance training?

At minimum annually, but quarterly updates on significant regulatory changes are highly recommended.

The Bottom Line: Comprehensive Compliance Protects Your Agency

Compliance isn't a "set it and forget it" task. Staying current with Regulation F is crucial, but understanding and adapting to state-specific debt collection rules is equally vital. Ignoring these complexities can lead to expensive legal battles, consumer reporting agency disputes, and reputational damage.

Still playing compliance roulette?

Reg F is just the beginning. See how agencies using Aktos eliminate risk with real-time, automated compliance—across all 50 states.

👉 Book a demo with Aktos and stay ahead of every rule change.